This piece was written in the fall of 2016, but many of its core lessons remain true to this today. In some cases, moreso than when they were written.

The following is an excerpt from Investment Management Associates’ second-quarter letter to investors.

The Great Recession may be over, but seven years later we can still see the deep scars and unhealed wounds it left on the global economy. In an attempt to prevent an unpleasant revisit to the Stone Age, global governments have bailed out banks and the private sector. These bailouts and subsequent stimuli swelled global government debt, which jumped 75 percent, from $33 trillion in 2007 to $58 trillion in 2014. (These numbers, from McKinsey & Co., are the latest we have, but we promise you they have not shrunk since.)

A lot of things about today’s environment don’t fit neatly into economic theory. Ballooning government debt should have brought higher — much higher — interest rates. But central banks bought the bonds of their respective governments and corporations, driving interest rates down to the point at which a quarter of global government debt now “pays” negative interest.

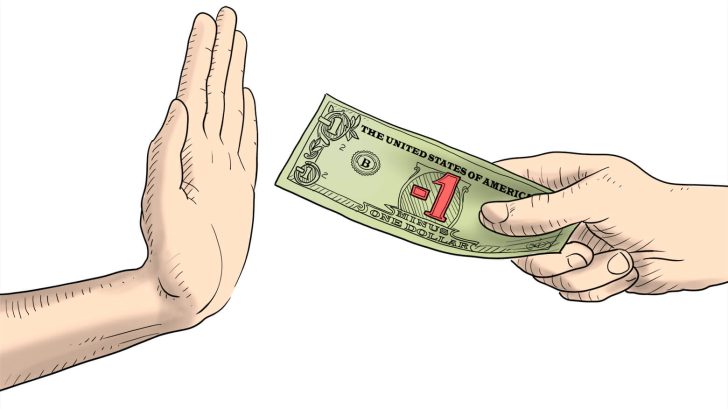

The concept of positive interest rates is straightforward. You take your savings, which you amass by forgoing current consumption — not buying a newer car or making fewer trips to fancy restaurants — and lend them to someone. In exchange for your sacrifice, you receive interest payments.

With negative interest rates, something very different happens: You lend $100 to your neighbor. A year later the neighbor knocks on your door and, with a smile on his face, repays that $100 loan by writing you a check for $95. You had to pay him $5 for forgoing your consumption of $100 for a year! Try to explain this logic to your kids. We tried to explain it to ours and failed, miserably.

The key takeaway is this: Negative and near-zero interest rates show central banks’ desperation to avoid deflation. More important, they highlight the bleak state of the global economy.

In theory, low and negative interest rates were supposed to reduce savings, get consumers off their butts and stimulate spending. In practice, the opposite has happened: The savings rate has gone up. As interest rates on their deposits declined, consumers felt that now they had to save more to earn the same income. Go figure.

Some countries resort to negative interest rates because they want to devalue their currencies. This strategy suffers from what economists call the fallacy of composition: the mistaken assumption that what is true of one member of a group is true for the group as a whole. As a country adopts negative interest rates, its currency will decline against others — arguably stimulating its export sector (at the expense of other countries). But there is absolutely nothing proprietary about this strategy: Other governments will do the same, and in the end all will experience lowered consumption and a higher savings rate.

The following point is so important we want to repeat it, in bold: If our global economy were doing great, interest rates would not be where they are today!

As we zoom in, things get worse. Let’s start with Europe, the world’s second-largest economy. European political (EU) and monetary (EMU) unions were great experiments that made a lot of sense on paper. Europe, which had roughly the same-size population and economy as the U.S., was at a competitive disadvantage as dozens of currencies embedded extra transaction costs in cross-border trade, and each currency on its own had little chance of competing with the U.S. dollar for reserve currency status.

There were also important noneconomic considerations. Germans were haunted by their past; they had started two world wars in the 20th century, and a united Europe was their way of lowering the risk of future European wars.

Economic and Monetary Union sounded like a very logical marriage of all the significant powers of post–World War II Europe, but the arrangement was never really a marriage. It was more like a civil union. EMU members combined their currencies into one, the euro. They agreed to use the same central bank and thus implicitly guaranteed one another’s debts.

Though treaties put limits on budget deficits (limits that, ironically, Germany was the first to exceed), each country went on spending its money as it wished. Some were relatively frugal (like Germany); others (Portugal, Ireland, Italy, Greece and Spain) went on spending binges, like newly hitched college students who had just gotten their first credit card, with an irresistibly low introductory rate and a free T-shirt.

The European Union is a collection of states that are vastly different from one another. They are separated by culture, language (which impedes labor mobility, resulting in semipermanent labor productivity disparity between countries — think Greece and Germany), economic growth rates, indebtedness and history. Germany, for instance, suffered through hyperinflation in the early 20th century and is thus paranoid about inflation.

Now let’s turn to Brexit, the U.K. referendum on exiting the EU. Ironically, the U.K. doesn’t have half the problems that most EU nations are going through. Because it is not part of EMU, it has retained its currency and its central bank.

The U.K.’s main dissatisfaction with EU membership stems from the immigration issue. Because treaties have turned the EU into a borderless union, when Germany accepted refugees from the Middle East and Northern Africa, it basically made a unilateral decision on behalf of all EU members to accept those refugees to all EU countries. High unemployment, wage stagnation and terrorism are now endemic in the EU, and you can see how the U.K.’s citizenry might have a problem with this.

After the Brexit vote, the financial media lit up with opinions on its consequences for the EU and the global economy. They’ve varied from “Brexit is a nonevent” to “This is a Lehman moment for the global economy,” referring to the Lehman Brothers bankruptcy that almost brought the financial system to a halt in 2008. The arguments on both sides are quite convincing.

The argument for Brexit’s being a nonevent is simple and straightforward. The U.K. maintained its currency, and the pound’s decline in the aftermath of the referendum will help cushion any negative fallout on the British economy. The U.K. and the EU will forge new trade treaties. There is a fear that the EU may impose trade sanctions on U.K., not so much to punish the U.K. but to threaten other EU members that exit will come at a stiff economic cost (effectively turning this voluntary club into a prison). However, the U.K. is a net importer of goods from the EU; thus any sanctions will hurt remaining EU members more than the U.K.

The Lehman moment argument is less simple, but not unimaginable. Brexit may provide the spark that will ignite already gasoline-soaked ground. Though the EU and EMU were supposed to unite Europeans, they may have had the opposite effect — causing a groundswell of nationalism.

In all honesty, we are concerned more about Italy than the U.K. Italy is the third-largest economy in the EU, and its debt stands at 132 percent of GDP, second only to Greece (171 percent). Seventeen percent of Italian bank loans are noncurrent. In the depths of the financial crisis, that number was 5 percent in the U.S. Italian lenders account for nearly half of bad debt in the EU (source: WSJ).

If Italy was not part of EMU, it could just print lire and bail out its banks. But it gave up that luxury when it joined the single currency. To make things worse, in 2014 the EU passed a law that prohibits governments from bailing out their banking systems; thus the shareholders, debtholders and depositors may bear the brunt of the eventual bailout. Unless the EU passes a new law that bends the 2014 law — or the Italian government takes matters into its own hands, violating EU rules — we may see Italian debtholders and depositors hit with the cost of bank bailouts take to the streets and demand “Italexit.”

Nationalism is a highly emotional, zero-sum, us-against-them sort of business. Add immigration concerns on top of economic ones, and it’s not hard to see how Europe has turned into a highly combustible mixture looking for a match. And because emotions are often antilogical, future decisions by EU countries may not necessarily be beneficial to the European Continent.

Given that the situation in Europe is so complex and combustible, we don’t know whether Brexit will be just another match that simply burns out or the one that starts the fire. Will it trigger other exits? Will it slow down EU growth, thus straining an already leveraged system? We don’t know, and nobody does.

China is the third-largest economy in the world and is living through the largest debt bubble we’ll probably ever see in our lifetimes. From 2007 to 2014, the country’s debt quadrupled, from $7 to $28 trillion (according to McKinsey). Over the same time period, its economy tripled, growing from $3.5 trillion to $10.5 trillion. These numbers are staggering, and they point to one indisputable fact: All Chinese growth since 2007 came from borrowing. There was no miracle in it.

But it gets worse, much worse. The numbers also show that every $1 of new debt brought only pennies of GDP growth. In the absence of skyrocketing debt, the Chinese overcapacity bubble, which was already fully inflated pre-2007, would have burst years ago.

As the government continues to engineer growth by borrowing, every yuan of debt will bring less growth. The laws of economics have not been suspended in China. American economist Herbert Stein’s law states that things that cannot go on forever, won’t. When its debt bubble bursts, China will turn from being a tailwind for global growth into a headwind.

This brings us to Japan. It is the most-indebted developed nation in the world, with a debt-to-GDP ratio of more than 230 percent. Japan is the proof of Stein’s law — its economy is still suffering a hangover from what at the time seemed like an endless real estate party (bubble) that lasted from the mid-1980s into the early ’90s. Japan has been on the quantitative easing and endless stimulus bandwagon longer than anyone else and has nothing (well, except a lot of debt) to show for it.

Japan also has the oldest population in the world — 26 percent of its people are older than 65 (in the U.S. the figure is only 15 percent). Rising debt and an aging population are a double negative for the economy, as debt per capita is rising at an even faster rate than total debt. And since the working population is declining at an even faster rate than the population as a whole, debt per working person is growing at an even faster rate.

From what we just told you, you might think Japan is paying the highest interest rates in the world, somewhere in the high teens. Wrong! The Japanese ten-year bond yields negative interest.

We just spilled a lot of digital ink to give you a brief overview of what we see around the world. We did not do it to increase your consumption of alcohol or antianxiety medicine.

We did it for a few reasons. First, we wanted to show you that stock market performance has not been driven by the improving health of the global economy. Just as negative interest rates are not a positive for the continued health of the economy, current stock market performance does not augur rosy future returns for stocks. In fact, the opposite is true. The bulk of the stock market gains are because of one variable: the expansion of the price-to-earnings ratio. S&P 500 earnings have stagnated since 2014.

Stock prices have gone up because the Federal Reserve and other central banks have squeezed all investors to the right side of the risk curve. Stocks, and especially high-quality ones that pay dividends, are regarded as bond substitutes. Investors now look at the dividends of those stocks and compare those yields to what they can earn in Treasuries. This strategy will end in tears, as these bond-substitute stocks are significantly overvalued (Coke, anyone?).

Secondly, we wanted to show you the headwinds we are facing and what we are doing to avoid having them deflate the sails of your portfolio. Summarizing, these headwinds are:

• The risk of lower or negative global economic growth. If we get higher economic growth, we’ll treat that as a bonus.

• Something-flation. Inflation (high interest rates), deflation (low interest rates) or screwflation (higher interest rates and deflation). We don’t know which of these extremes we’ll see and in which order. Nobody does. Despite their eloquence and portrayed confidence, financial commentators arguing one or another extreme point of view on CNBC don’t know either. In fact, the more confident they are, the more dangerous they are. The difference between us and them is that we know we don’t know and are therefore trying to construct an “I don’t know” portfolio that can handle any extremes.

Ultimately, stock valuations will decline.

This is a time for humility and patience. Humility, because saying the words “I don’t know” is difficult for us testosterone-laden alpha male money manager types.

Patience, because most assets today are priced for perfection. They are priced for a confluence of two outcomes: low (or negative) interest rates continuing where they are or declining further, and above-average global economic growth. Both happening at once in the future is extremely unlikely. Take one of them away (only one!), and stock market indexes are overvalued somewhere between a lot and humongously (we don’t even try to quantify superlatives).

Read this before you buy your next stock

Key takeaways

- Central banks’ desperate policies have led to negative interest rates and distorted investor behavior, fueling a global Searching for Yield? mentality.

- Global debt has surged since 2007, creating systemic fragility in Europe, China, and Japan.

- Europe faces nationalism, Brexit uncertainty, and Italian banking risks that could destabilize the EU.

- China’s growth rests on unsustainable borrowing, while Japan struggles under debt and demographics.

- Investors should build resilient, “I don’t know” portfolios—embracing humility and patience instead of chasing risky yields.

")

comments

0