I wrote the following essay two years ago, but I want to share it with my readers again. I put this essay into the Public Service Announcements category. If you read it before, you can skip directly to the postscript at the end of the article.

Some of my colleagues at IMA advised me not to publish the essay you are about to read. They thought it would put me in the middle of political tribal warfare and I’d just frustrate a large group of my readers with it.

However, in the essay I shared with you a few days ago, I reminisced about having spent 30 years in America. I wrote:

Tribalism in the US has become so strong that it has started to impact our freedom of speech. No, the government is not going to send you to the gulag for your political thoughts. We do it to ourselves by canceling each other. …

How many of us now find ourselves afraid of being cancelled, or just don’t want to get into mindless, vitriolic debates with tribal drones (people who just repeat the talking points of their tribes). The more we self-censor, the less free we become.

Despite my colleagues’ insistence, I decided that I was not going to self-censor. Some readers might decide to stop reading my essays – well, they’re welcome to do that.

What is the point of living in a free country if you are afraid to voice your opinion? Actually, in this case it is not even an opinion, but rather analysis with investment consequences.

I made a deliberate decision not to belong to a political party. I don’t want to outsource my thinking to a collective. I am innately leery of groupthink – a useful trait in my day job as an investor.

The Slippery Slope of Student Loan Forgiveness

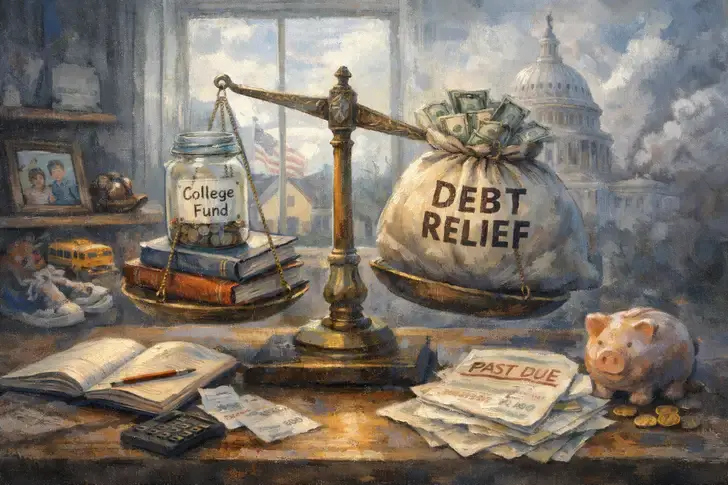

My wife Rachel and I had our son Jonah in 2001. I was 28 and she was 23. Rachel quit her job and became a stay-at-home mom and part-time student at CU Denver, where she was finishing her bachelor’s degree.

Both Rachel and I immigrated to the US ten years earlier, from the USSR. Now, I had a master’s degree in finance and a CFA license but was just a few years into my career as an analyst. I was working for a small investment firm, IMA, making $40,000 a year. As soon as Jonah was born, we opened a custodial educational account and started saving $2,000 a year for Jonah’s future education.

This $2,000 in 2001 was an enormous amount of money for us; it was around 7% of my after-tax income. We had a very modest lifestyle. We were still paying off our college debt. This education money could have let us afford to eat out, enjoy a daily trip to Starbucks, or take another vacation or two. We bought used cars, drove them for decades. We made a budget and lived by it (I wrote about it here). We felt it was our responsibility as parents to make sure that our son went to college and was not burdened by college debt. The value of education had been drummed into our heads by our parents. We wanted to give Jonah every advantage he could get in this country.

We opened similar education accounts for our daughters Hannah and Mia Sarah when they were born in 2005 and 2014. Though my income was growing as my career advanced, funding these accounts was always an effort. We needed more bedrooms – we bought a house. Also, when storks bring babies, what follows are unending new expenses: diapers, daycares, after-school activities; and the kids keep growing, so they constantly need new clothes.

As I look back at those years, though they were often trying, they were some of the happiest of our lives. This is the behavior I’d want my kids to replicate: Live within your means. Don’t get into credit card debt; pay off debts quickly. Save for a rainy day. Create a budget – which is basically categorizing and mindfully allocating your spending to things that are important to you. But making sure you take care of your kids’ education is at the top of the list. In advice to my kids, I’d throw in some Stoic wisdom, in that happiness comes from wanting what you have. Once your basic needs are taken care of, material things bring little happiness.

And then…

President Biden, with an executive order (a decision that did not go through Congress) “forgave” $10,000+ of many students’ loans. Aside from the fact that every member of my household, including my 8-year-old daughter Mia Sarah, is now on the hook for about $1,000 for this “forgiveness”, it felt like what Rachel and I were trying to teach our kids is now thrown out the window.

As I promised you, this is not a political essay, so here’s the analysis part.

This loan forgiveness is a very dangerous, slippery slope. Some will argue it started with Uncle Sam bailing out the big banks during the Great Financial Crisis. That is debatable, and there are a few important differences: The government did not “forgive” the banks or give them money but provided high-interest loans. Uncle Sam came out ahead in the end. Arguably, if the US had not bailed out its financial institutions, our whole economy would have crumbled. However, I am aware these nuances are somewhat lost, as the public looks at the government’s actions as a bailout. This sets a dangerous precedent. Yes, the government came out ahead, but it could have lost money.

Then, during the pandemic, the government opened the door wide-open by throwing trillions of dollars at anyone and anything with a bank account with a multi-trillion-dollar PPP shower. Arguably, this was necessary in the face of a global emergency, though the magnitude and follow-up stimulus are open to debate. Although this time around the government wanted to make sure that everyone got the money (not just the fat cats on Wall Street), due to its ineptitude a lot of this money was misappropriated. Some were showered with more PPP money than others.

Now today, anyone who went to college, has student loan debt, and makes less than $250,000 a year (per couple) receives “forgiveness” from Uncle Sam and my daughter Mia Sarah.

This executive order doesn’t even attempt to fix the core issue of runaway inflation in college tuition. In fact, it will likely make tuition inflation even worse by throwing more taxpayer money at colleges and lead to endless “forgiveness” in the future.

But what about the plumber or truck driver who never went to college and thus has no college debt to forgive? This where the slippery slope turns into a giant landslide. They are next. As interest rates go up, people go upside down on their houses and mortgage interest cripples them. No worries, Uncle Sam and Mia Sarah will come to the rescue; they’ll forgive those loans. But what if you are not lucky enough to own a house but have a mountain of credit card debt? Don’t worry, you’ll be absolved of those sins, too – you won’t be left behind.

In the meantime, people who are like Rachel and I were 20 years ago, folks who give up vacations, new cars, Starbucks frappuccinos and Chipotle burritos to save for their offsprings’ education are incentivized to do the opposite. Why bother?

Making choices as to what college to attend, selecting a major, and deciding how much debt to take on falls into the personal responsibility bucket, too. When the government decides to forgive student loans (and then, maybe, mortgages and credit card debt), that is a plain-vanilla wealth transfer to those absolved from their debt (their past choices) from the rest of the society, who made painful, responsible choices, and from future generations (the Mia Sarahs and those who are yet to be born).

The US has earned the right for its dollar to be a world reserve currency. It was earned because we had the strongest free market economy. There is a very good reason why most innovation doesn’t take place in Europe but in the US. We are the country where people want to take risks, enjoy the fruits of their successes, and pay the price of their failures. A free-market economy cannot exist without failure, just like heaven cannot exist without hell.

The reason companies fail, and empires collapse is simple – they become arrogant. They forget that their success was earned by sweat and paranoia. They start taking it for granted. They become fat, lazy, and happy. Just like companies and empires, the US is not absolved from the laws of economics.

As our government adds more debt and probably raises taxes, inflation will not be transitory but will become a nightmare of everyday life, and our economy will weaken. With every “forgiveness,” the US dollar will become a less attractive currency, as it will buy fewer and fewer goods. It will be less differentiated from the currencies of other troubled countries.

As an investor who is hired to preserve and grow my clients’ nest eggs, I’m finding, unfortunately, that diversifying away from the US dollar is becoming a responsible thing to do.

Postscript: My daughter Hannah was just accepted to University of Denver. She might take out student loans. Why wouldn’t she? The government will forgive them anyway. More importantly, millions of other “Hannahs” will do the same. Yes, there are unintended consequences to government actions.

Post-postscript: Countries don’t degrade overnight; the change happens slowly, one loan forgiveness, one giveaway, one social redistribution at a time, and then it happens overnight. You wake up one day and don’t recognize the world around you.

A century ago, Argentina was one of the wealthiest countries in the world. Yes, you read that right. Buenos Aires was built by Europeans; it looks like Paris and is often called the Paris of Latin America. As its success went to its head, the socialists took over; they started to take past success for granted as a God-given right. Argentina went from one of the richest countries to a poor one, enduring high-inflation bouts every other year. (I hope Milei changes its course.)

Nothing precludes us from becoming another Argentina. Absolutely nothing. Argentina’s decline did not happen overnight; it took decades.

Today, the US dollar’s status as the world’s primary reserve currency is what allows us to run insane budget deficits and do forgiveness giveaways – while the economy is not in a recession. But the “exorbitant privilege” accorded the US dollar is the fading legacy of our past success. Our current behavior is not worthy of the trust the world places in our currency. At the moment, the world doesn’t have better alternatives, but slowly, countries will start diversifying to other baskets of currencies or commodities. Again, these changes happen slowly, and then very fast.

Key takeaways

- The recent student loan forgiveness policy undermines the values of personal responsibility and financial prudence that many parents, like yourself, have tried to instill in their children through sacrifices and careful planning.

- Student loan forgiveness sets a dangerous precedent, potentially leading to a slippery slope of other debt forgiveness measures (mortgages, credit card debt) that could weaken the economy and devalue the US dollar.

- The policy fails to address the root cause of rising college costs and may actually exacerbate tuition inflation by injecting more taxpayer money into the higher education system.

- Student loan forgiveness represents a wealth transfer from responsible savers and future generations to those who benefit from debt absolution, potentially discouraging prudent financial behavior in the future.

- The cumulative effect of policies like student loan forgiveness could gradually erode the strength of the US economy and the dollar’s status as a world reserve currency, drawing parallels to the economic decline of countries like Argentina.

")

Absolutely spot-on essay – You stated the key point so well here: “‘The reason companies fail, and empires collapse is simple – they become arrogant. They forget that their success was earned by sweat and paranoia. They start taking it for granted. They become fat, lazy, and happy.” This same warning has been sounded for millennia – by such sage voices as Moses in Deuteronomy; by Ibn Khaldun in the 14th century Muqaddinah; and by Solzhenitsyn when he famously said, “Prosperity breeds idiots.” My next book will explain why this happens – titled “The Great Forgetting: How Prosperity Corrodes Wisdom and Breeds Intellectual Folly.” The more things change . . .

I think many of your readers are disposed to accept your arguments on student debt forgiveness due to the fact that we follow your thought and analysis because we tend to agree with it. And indeed, I fully appreciate the points you are making. But there is another side to the issue that should be considered.

The student debt forgiveness can be seen as nothing more or less than a federal government subsidy for higher education (a subsidy Congress has never voted for, which raises the question of the constitutionality of this act now being tried in court). But such a subsidy can be seen as an investment in ongoing competitiveness of the American economy. In my field of engineering, I see legions of Chinese and Indian engineers filling demand for all sorts of technical needs of American consumer products companies. It is not irrational to think that all of us as taxpayers should be willing to make careers dependent on higher education easier to attain, particularly for children of poor families who are not necessarily less intelligent than children of well to do families. In my (Republican) state of Georgia there is a device called the Hope Scholarship Fund that uses revenues taken from legal gambling (the lotteries) to provide, conditionally, a tuition subsidy. This was passed years ago by the Legislature and has continued with bipartisan support. It is run by the Georgia Student Finance Commission with the stated purpose to “…ensure Georgians have an opportunity to access education beyond high school.” and is one approach to the issue at hand.

Now it can, and should, be argued that improving the cost effectiveness of American higher education should be a top priority in terms of public policy as the costs of higher education have outstripped inflation by an astounding amount.

My takeaway on student debt forgiveness is that this is something being tried in the wrong way for the right reasons.

Truly outstanding article, 1000 % agreed, we are on the verge of losing the Republic due to the “Tribe” responsible for this. Thank you Vitaliy !!!

While I agree that loan forgiveness as stated in your article may be well meaning, but possibly unfair to people who have paid off loans or to students or parents that paid in full so their children didn’t need loans, how about an article /analysis on loan forgiveness programs that do make sense. Programs that forgive loans for people who teach or open medical related practices in low income underserved areas or ‘Special Needs’ students? Also you briefly alluded to actions not being taken against Universities. Predatory ‘For Profit Only’ schools . Programs of Forgiveness for students of those schools should include Clawback provisions and the schools to be removed from receiving loan payments in the future unless they can show/prove their graduates can obtain jobs/careers that can provide adequate incomes to payback loans in a reasonable time frame. Additionally any school should be required to only receive loans for educational programs based on the compensation a student’s chosen field may provide over for example a 10-20 year period.

Basically when are there times that Loan Forgiveness makes financial and Societal sense

Could not agree with this article more! I have recently wrote to President Biden saying something very similar. Unfortunately, I cannot support him because of this. I can’t accept the fact that I am paying for people’s student loan debt that make more than I do every year. If you are making a combined $250k a year and can’t pay your bills, something else is wrong.

Worked in college library and dining hall. Worked part time in hospital dietary dept.

Lived at home, went to college year round.

Completed 79 credits in 20 months. Deans list.

Had $1100 in student loans, paid off in two years.

No frills, no regrets.

Damn proud of you for your “no fear” essay.

You are right-on sir, and I agree with you 100% I graduated from TAMU in the late seventies with some student loan debt and it took me and my wife about two years to pay it off. It was an obligation that we didn’t give a second thought to but we did celebrate when that last payment was made.

Thank you for all of your letters.

there’s just one thing wrong with your essay. despite the name, the loan forgiveness program doesn’t just forgive student loans if you make under 250k etc. they require student loans borrowers to give them access to their tax returns every year for up to 25 years. if they do not make more than a benchmark poverty level then they don’t make them pay. the amount they pay depends on how much they make. many of them are doing good work for society they just don’t make much money.

I would love to see a fair-minded econometric study of the redistributive effects of SL forgiveness.

I’ll reserve judgment until such a study but every bit of economic intuition I have tells me the redistributive effects of SL forgiveness are to take from the poor and give to the better off. How is that consistent with the stated beliefs of the ruling party?

the unfairness of it all

yes Hannah can take out loans at 9% (banks make nice $) that the government guarantees. Student debt is one of the few areas that can’t be washed away by bankruptcy. Yes Hannah might have 10k forgiven of her yearly 80k cost

You don’t begrudge fire or plice departments that spend taxpayer money. Concept is those services are a public service. I’d offer that an educated populace is good for the country. If we truly don’t want to burden the taxpayer let’s eliminate public education altogether.

Part of the concept is that students coming out with huge debt can never participate in the economic engine, they spend decades trying to get back to neutral. The logic of spending hundreds of thousands of dollars on an education in art appreciation so you can become a barista is a good conversation to have with your high school senior. Our government subsidizes many things: farmers not to grow crops, oil companies, sport stadiums, real estate depreciation, EV cars, corportions that pay basically NO taxes: Ford, GM, ATT, Chevron. So subsidies are out there…..why are students different than these other groups?

As to fairness, Hamilton faced this 250 years ago when he decided the Federal Govt should assume revolutionary war costs for ALL states. those that owed loved the idea, those that had basically retired their state debts screamed bloody murder. So this is nothing new.

I’d suggest rather than rail against communism or tribalism why not a discussion of the the issues, problems, goals and potential approaches

What is never brought up is the issue of people put into horrible medical debt with cancer. Even people who did everything right and even had good insurance could get wiped out if extensive treatments exceeded their max coverage. Someone is this scenario can be financially ruined through no fault of their own. Isn’t that a more worthy option for relief than voluntary college debt?

Thank you Vitaliy for not self-censoring. I and many, many others lived similarly. We didn’t know we had any other options… and we’re the better for it. I put three kids thru college like you. They started without cars and lived in dorms. They all graduated, handle money well and are successful in life. In their early days of college, I could not figure out for a while how so many college kids could afford such nice cars and lifestyles. But the college loan scam eventually became evident. And as I’m sure you understood too, I knew that gig would end badly for many… just like the 2000’s housing crisis. But the worst harm is not the waste of money, but the damage that entitlement and failure to take responsibility is doing to our youth and nation.

As you allude to though, if the US dollar ever ceases to be the reserve currency, all will be forced to learn what all U.S. citizens used to understand about money and economics.

Keep up your good work Vitaliy and may you never self-censor!

Good article: The loans to the students are made by banks. Repayment is guaranteed by the Federal Government. The forgiveness of the student loan does not negate the obligation of the Federal Government to reimburse the banks. Therefore, the general public, you and I, will be paying for these loans. Thank you for your articals

Hi Vitaliy,

I understand your point of view, but I’ll give a little bit of a gentle push back on it. It will help to understand my story, just briefly. I graduated from high school in the 1970’s when, realistically, only the class valedictorian, and perhaps the salutatorian, received substantial academic scholarships. College, for me, was a financial impossibility even though I graduated in the top 10 percent of my class. My mother had died years earlier, my Dad had remarried, but he was the only breadwinner for the family. He worked very hard, but it was only enough to keep us in food and shelter. I was actually able to buy my own clothes. When my step-mother appeared on the scene, she realized that the children from my Dad’s first marriage were eligible to collect Social Security. So, in a way, because my parents let us have complete control of the money, they were somewhat helping us save for college. It wasn’t much, but I was the frugal kid. I kept plowing money into savings bonds, but it just wasn’t enough. I visited a few college campuses, but the costs were way beyond my means. No further help from the family coffers was available.

So, just past my 18th birthday, I decided to start visiting the recruiting stations for the Armed Services. The first one was the Air Force, but I made note of their very negative reaction to my answer to their first question. They had asked me what I wanted to get out of my time in the Air Force and I promptly answered “an education.” It was a very honest answer – I had really wanted to go to college. The rest of the interview was beyond awkward and I could see that this would never work. More determined, the very same day, I dropped by the Navy recruitment office. Darned if they didn’t start out with the very first question. I stopped short and told the recruiter about the reaction to my answer to the Air Force. I was going to give him the same answer and I basically told him so. He was encouraging and his response was “Hey! The Navy loves people that want to further their education! That’s a good answer and the interview did go very well. When he found out that I was doing well in school and that I was best in science and math, he could barely contain himself. They had me take the ASVAB and I scored rather well. (word knowledge was weak though). He said, if you have 20 minutes or so, I’d really like you to stay and watch this film we have. He sat me down at this machine that only played one tape. It was “Underway, On Nuclear Power!” narrated by none other than Captain Kirk himself (yeah, the Shat! William Shatner). The next thing I knew I’d signed up for six-year obligation for the nuclear navy.

But, … the Vietnam war had ended and Congress pushed to do away with the GI Bill. They soon realized their mistake (it really impacted recruiting) and brought it back just 18 months later. Unfortunately for me, I fell into that 18 month window when it had been replaced by the Post Vietnam Era Assistance Program. Each branch of the service had their own program and the Navy’s was a bit less generous than the others. I made use of it in what was called the Navy’s 2 for 1 Program. For every dollar that I contributed to a savings fund for college at a later date, the Navy would add $2 to it. At the end of my six-year enlistment, I could put the total toward my own education. With inflation, that wound up being about a year and a half of college. In addition, I send most of my paychecks home to simply stash away in my hometown bank account. The first two years I progressed through Navy schooling and then I spent four years on sea duty. If I lived on base or on the ship, then my expenses were minimal since I’d be fed and I had a place to crash.

After my six years were up I had decided it was my time for college. Financial aid was now based on just my income and savings (and the income had stopped). I wasn’t eligible for much since my savings were enough to get me through for a while. Since I had just come off of active duty, I didn’t think I had to register for the draft, but guess again. Before I was eligible to apply for financial aid, I had to! The savings drained away quickly and the need for loans cropped up. I wasn’t about to stop, so the loans were a necessity. That was okay for about a year when three gentlemen from Washington, DC came up with the brilliant idea of making student immediate begin paying interest on their student loans. This meant that I had to borrow even more so that I’d have the extra money to begin paying interest on the loans. Whee! Further in debt! I managed to graduate cum laude after just 2 years and 9 months and started a masters program a week later. A year after that I finally entered the workforce again earning barely enough to take care of necessities and to start paying down my loans six months later. The shock that I got was that the Gramm Rudman Hollings loans were not able to be combined with my other student loans and for the first five years or so I had to budget for both loans. That forced me to give up my nice apartment and move into subsidized housing where I was pretty much the only one paying my rent (too “wealthy” to be subsidized myself). I moved to a better paying position not long after that.

I was nearly 40 years old before my student loans were finally paid off. With all of that experience, you might think I’d be very much against student debt relief (and I doubt many would blame me if I was). However, I thought beyond just my own little fiscal world. I knew the pain of getting out from under that debt. I didn’t really want others to experience that just because I had. Also, it seemed as if the loan terms that students were getting were a lot worse than what I had experienced years ago. Yeah, on the surface it isn’t fair that a large percentage of those with no debt would help the smaller percentage with student loan debt. However, what if you’re working a trade and your service/company/trade relies on other Americans buying your products or services. How many of these folks stuck with student loans (with outrageous terms) could be buying from you if they just had some relief. Maybe it’s time for that new roof or to put on that deck or get that newer car. The benefits to others are real and can be felt. The money not spent on loan repayments will usually get plowed right back into the economy or saved for THEIR children’s education. We could consider how to help them end the circle of poverty.

Or, we could let them continue to twist in the wind. It’s their lot in life if they came from nothing and got stuck with seedy, non-negotiable, greed-seeped loans when they dared try to break out of poverty with an education. Too bad on them I guess? No, I don’t buy that argument. We can all benefit by helping them past this insidious student loan industry.

I can certainly understand your point of view to a point, I just think it’s a little short-sighted and lacks awareness of what the student loan industry is getting away with.

“What is the point of living in a free country if you are afraid to voice your opinion?”

I agree.

A travesty, and on the same page … a few thoughts:

1) This is (also and foremost) all about politics, and buying the youth vote – period

2) It’s disgraceful, and is changing nothing to the “structure” of the system – as I said, check out 1)

3) We live in a YOLO world – why bother about the future, since “climate change” = doom, so: we don’t marry, we don’t have kids, we live in the moment, and life becomes a meme, take as much as you can from society …

4) The US $ is the least dirty shirt, but others will take over the reigns in due time – ALL fiat currencies have collapsed at some point in the past, and will continue to do so. HODL becomes more attractive by the day

5) “Always expect the unexpected” (Backyardigans)

6) “At some point, you run out of OPM” (Margareth Thatcher)

(bonus) I’m sending/have sent my 2 boys to go and study in Europe – the best financial arb any family with kids should consider: cents on the $; rich cultural environment (none of the sh.. we have here); focus on study first (not the extras…); merit based (none of the sh… we have here); and no cancellation if you happen to utter the wrong pronoun … oh, and no lawsuits on every other turn.

Anyway, you catch my drift.

Keep writing/sharing, love your work.

Let’s grab a drink when you’re in town next (tri-state area).

This is kind of a reductive view of the situation. Lots of the forgiveness has gone towards people who were in some way defrauded or misled by their institution. Much of the forgiveness will go towards public servants who are arguably a good return on investment (and don’t have access to signficant upside in their professions).

People take issue with the “bailouts” during the GFC because they were used to prop up institutions and individuals that engaged in reckless speculative behavior. Portraying seeking higher education as speculative or reckless is not accurate for the most part. A common tribal trope seems to be along the lines of the 250k student debt forgiven for the Renaissance Fair major or something equally absurd. You’re couching it in terms of “why wouldn’t I take on debt then” but 10k of forgiveness is not going to cover a significant amount of the cost of most 4-year degrees.

You mention truck drivers and plumbers not benefitting from this process and how their next. This seems to be a common tribal trope that you’re also amplifying that pits different demographics within the middle class against each other. But a plumber may attend a trade school eligible for federal loans that may be forgivable at some point. Arguments like this always seem to ignore the massive handouts enshrined in the system to businesses through tax breaks and loopholes which in my view are akin to forgiveness.

As a society I think we would agree that using travel and dining as business expenses to reduce the amount of taxes you pay probably doesn’t provide nearly the return on investment that forgiving some amount of loans for a teacher who is paid below the median wage in their area. I don’t think our society is moving towards removing personal responsibility because we want to make education more accessible.

I am 100% in agreement with what you said here in this essay, and also with others on similar “tribal” topics such as the inevitable and ongoing negative impact of union ownership of certain state governments such as the one I live in, California, as well as ownership of the current holder of the Oval Office. Thank you for speaking out, and i have shred your essays numerous times over the years, as well as your book “Soul in the Game”.

Vitaly,

Excellent essay! Good for you for publishing it, and shame on your colleagues for discouraging you. We need more people like you to speak out and be in Washington, but alas that will never happen because of our broken political system. How can anyone argue with your thoughts on where we are headed? But how can politicians get elected if they endorse the tough decisions that we will have to make to get our economy back on course?

Thank you for taking the risk and telling the truth.

I earned the money to pay for my education and then paid for our children as well. And we helped with grandkids too.

People need to speak up without worrying about those who disagree.

The only things in life that are free today are not related to money. This includes freedom of speech and the freedom to make choices.

Great article on point. I too left the political parties in this country long ago. If we keep electing these leaders we will end up like Argentina.

Very well said Vitaliy! Should be required reading for every liberal

I agree with your comments 100%. I paid for my college degree and my son’s college. Transferring college debt to people who either paid their own debt or didn’t go to college seems criminal. In any event, transferring someone else’s debt to others doesn’t solve anything long term. It certainly doesn’t make college cost any better.

So gently and calmly but firmly spoken. Speaking so others listen and buliding communicatin bridges is so important.

Yes, “free money” is aweseome, but we all know it is not free (or do we?) Thank you for including that Mia is paying for loan forgiveness, too – it’s powerful image that sticks with the readers.

Thanks!

Vitaliy- I really enjoy your writing. Would have been great to see this article advocate for free market reforms to student debt–since those are so close to your work and expertise. If student debt could be discharged in bankruptcy or priced based on what the student was studying (or where they were studying)–it would really help the situation, and likely eliminate most of the need for debt forgiveness. The reason it might be a good idea for your daughter to take on debt to fund her education is not that the debt might be forgiven, but that–if she chooses her studies wisely–education is a good investment. For the many that don’t have access to as good advice, some simple regulatory changes would help.

This article is excellent. I think very few understand how enterprises and societies rise and fall. The short-term perspective can make it hard to see long term consequences.

Watching my children’s fellow college students use student loans to attend concerts, travel, and throw parties always made me feel like these kids missed some parenting along the way. These same kids blew off classes and struggled to graduate. They made choices, they need to learn from them. Blanket forgiveness is rewarding these poor choices.

Amen! You should run for Congress to bring not-so-common sense to Washington.

To quote Dr. Zhivago after the housing committee seized his house, “Yes comrade this is much more fair.”

Biden and the democrats are now directed by the Communist wing of their party.

The problem as I see it is the easy money provided by the US government for student loans. An 18 year old, without the benefit of successful parents to guide them, is very, very easy prey to institutions that often exist for the sole purpose of collecting student loan money: These are primarily the “for profit schools” that after years provide little in marketable skills to its students while its students rack up huge financial debt.

Another problem is the runaway cost of higher education both private and public. Without Federal student loans, very few could afford the asking price of tuition. Without student loans, the lack of students who could afford would drive down prices.

Finally there must be a realization that a college experience that resembles a resort, complete with swimming pools, suites instead of dorm rooms. etc. will cost as much as a resort – while adding little to nothing to the education that one is supposed to receive.

When I went to a highly competitive college in the early 1960’s, three of us were in a room; the bathroom and showers were down the hall, when it got hot we opened the windows, there were no sport scholarships and financial add was available to those who qualified. Upon graduation over 90% got a job – we had to to support ourselves.

Thank you for having the courage to speak your mind, in an intelligent manner, on an important subject that may spark the anger of a “tribe”.

I’d almost agree with you except that !0,000 forgivemesss of a debt for college today is nothing considering the cost of a state scoool in my state is close to $0,000 per year. And when you and I went to school the interest rate on a student loan was 2-% and now the interest rate is at least 9%, a rate which doesn’t permit many students to do anything but pay the interest on their loans. They can’t get ahead.

Absolutely on target !

In nature, do you know of one single other species, than human beings, that obliges its youngsters to pay for their own education ?

I don’t.

And it is my view that this is not ethical, and that it is counterproductive in the long run, as too many people have to start their active life with a heavy burden, for too little adequate and well-paying jobs.