I wanted to share with you some edited excerpts from a Q&A session I held with readers in Omaha during Berkshire Hathaway’s shareholder meeting weekend. This email covers our approach to client management, how we decide on stock positions and how to interpret negative book value.

How do I deal with prospective clients who have a short-term time horizon?

At IMA, we handle this very differently. We do what I call “reverse marketing.” Here’s how it works: I write articles, people read them, and in these articles sometimes I talk about what we do. When people get interested in our services, they download our brochure and reach out to us.

In our brochure, we tell them exactly what we do and what we don’t do. They usually read my articles for years, then they read the brochure. In fact, they won’t be able to talk to any member of my team if they haven’t read the brochure. If they haven’t, we say, “We’d love to talk to you after you read the brochure.”

To be our client, you need three things. Number one, you need to have a long-term time horizon. Number two, you need to buy into our philosophy. And number three, you need to commit to reading my letters to clients. Three or four times a year, you’re going to get an email with a 20- to 30-page PDF attached. You have to read it. If you’re not willing to do all three of those things, you don’t get to be a client.

It’s a kind of reverse selection. We just don’t take clients who don’t buy into our approach. Sometimes, wrong clients slip in. We had a client who started with us in July, and by September he was writing to us, “Well, the S&P was up 8%, you were up 3%, what’s your excuse?” I wrote him a “Dear John” letter, explaining that he might have joined the wrong tribe.

This approach helps us filter out clients who aren’t aligned with our investment philosophy and time horizon. It’s better for everyone – us and the clients – if we’re on the same page from the get go. If someone’s looking for short-term gains or constantly comparing us to indices over a few months, they’re probably not a good fit for our strategy.

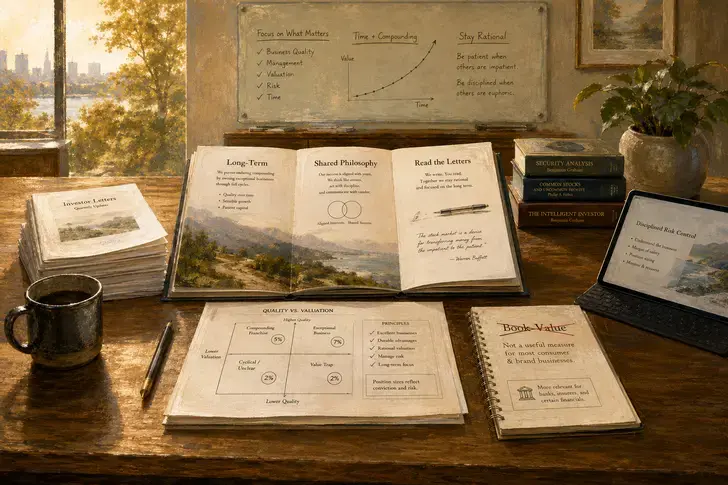

How do you decide your position on stocks?

Okay, think of it as a matrix. You have quality and valuation. Let’s say you have a very cheap, high-quality company – that’s a 5 to 7% position. Then you have low-quality and expensive, which would be on the opposite corner. It’s a spectrum.

First off, if it’s low-quality and overvalued, we probably shouldn’t own it at all. But you get the idea of the spectrum, right? Companies fall somewhere in this matrix, so we try to marry quality and valuation.

One thing to note: Quality doesn’t change as often as valuation. A high-quality company at one price might be a small position, but at a lower price it becomes a larger position. It’s price-driven, based on how undervalued it is. Take Uber. We started it as a 3% position and added to it when the price dropped.

In Uber’s case, I’d argue its quality has increased over time. Here’s the tricky part: We have an A, B, C, and D rating for each company. When we bought Uber, I thought it was an A, but then the quality improved. What’s better than A? A plus? A double plus? You see, there’s still a lot of judgment involved, but this is our general framework.

When I analyze a company and find the quality is too low, we just move on. I’ve learned that my emotional quotient isn’t very high with low-quality companies. We want to focus on high-quality and undervalued stocks.

Position size is usually capped at 5%, with rare exceptions going to 7%. McKesson was a 7% position because I felt I understood the company extremely well and thought the chances of permanent loss were almost zero. But those opportunities are rare.

Part of the reason for this approach is that we often manage most of our clients’ money. Many times, it’s all their investments. So we treat it as irreplaceable capital. When you’re young, you can afford mistakes because you have time to recover. But when you’re 60 and nearing the end of your working years, you can’t really recover from big mistakes.

So, we have this mechanical, quantitative position-sizing framework to protect me from myself. When you find a company, you can fall in love with it and get emotional, thinking it should be a 50% position. But it’s not, because things can always go wrong.

That’s why we have a portfolio with 4–5% positions, typically.

There are rare exceptions. Once we had a 50-basis-point position that was like a lottery ticket – 100x upside with 100% downside. But usually, 2% is our smallest position size.

This approach helps us balance potential returns with risk management, always keeping in mind that we’re dealing with our clients’ hard-earned, often irreplaceable capital.

What is your view of companies with negative book value?

Starbucks and McDonald’s both have negative book value, but it means nothing. In this case, negative book value just means the company has been buying back stock. The math is actually very simple.

When companies go public, shareholders’ equity basically reflects their stock issued at par, or maybe a dollar per share (I’m oversimplifying things a little). Then, over the next 20 years, their stock appreciates a lot, and so do their earnings.

When they buy back stock, for every share repurchased at, say, $50, which has a book value of one dollar, you automatically create negative $49 in book value “destruction.” So it’s completely meaningless.

If I owned Starbucks or Microsoft, I would never ever look at book value. It’s worthless for these types of companies. Think about what book value really is – it’s generally just the difference between assets and liabilities, right?

Now, the liabilities are more or less current, but the assets on the balance sheet often aren’t. The Starbucks brand, for instance, doesn’t really show up on their balance sheet. It’s intangible.

However, book value becomes important when you look at financial companies, because their assets and liabilities are marked to market all the time. So, if I’m looking at an insurance company or a bank, book value becomes a lot more relevant.

For companies like Microsoft or Starbucks, I promise you, not a single experienced investor knows or cares what their book value is. It’s a worthless number for these companies.

The key is to understand what metrics matter for different types of businesses. Don’t blindly apply the same metrics to every company you analyze. Focus on what truly drives value in each specific business model.

Key takeaways

- We practice “reverse marketing” — prospective clients must read my articles, commit to our brochure, and agree to read my quarterly letters before they can even talk to my team. If they won’t commit to all three, they don’t get to be a client.

- Firing clients is sometimes necessary. When a client joined us in July and was already complaining about short-term underperformance by September, I wrote him a “Dear John” letter. He had joined the wrong tribe.

- Position sizing follows a quality-and-valuation matrix. A cheap, high-quality company earns a 5-7% position; low-quality and overvalued names don’t belong in the portfolio at all. Most positions sit around 4-5%.

- We cap positions at 5% (rarely 7%, like McKesson) because we manage most of our clients’ irreplaceable capital. This mechanical framework protects me from falling in love with a stock and turning it into a 50% position.

- Book value is meaningless for companies like Starbucks, McDonald’s, or Microsoft — negative book value often just reflects years of buybacks. It only matters for financial companies, where assets and liabilities are marked to market.

")

comments

0