My Q&A session with CFA Society UK in London was recorded. I’m going to share with you the recording and a polished transcript. As I was editing the transcript, the writer in me took over and I added some additional thoughts. Fair warning: This reads like a transcript, because it mostly is.

I’ll break the transcript into two parts. Part 1 will focus on investing and living with intention. Part 2 will answer questions related to the AI bubble.

Part 1: Living and Investing with Intention

On Micro-Dosing Investments

About five years ago, at the beginning of the pandemic, you said: “I will micro-dose my investments to diversify away my ignorance.” How did that work for you, and what lessons do you take from it today?

Let me first explain what I do. I run an investment firm. Clients come to us and say, “Here are my life savings. Don’t screw it up.” What they mean is: I manage all their funds. When I make investment decisions, my number one goal is not to blow up—to make sure they get to retire.

In our investment process, we pay a lot of attention to risk. Since I’m talking to value investors here, for us, risk is not volatility. Risk is a stock going down in value and not coming back—permanent loss of capital.

To answer your question: When the pandemic started, I didn’t have a reference point. I had to go back 100 years to find something comparable, and I had no idea how it would work out. Would it last one year? Three years? Ten years? So I tried to create a portfolio that would survive no matter what.

I also realized there were unknown unknowns. If I made a decision that went bad, I wanted my exposure to be small. We usually run 20–25 stocks. At that time, we expanded to maybe 30 or 35, making each position smaller—micro-dosing decisions—because I didn’t want to blow up.

Let me give you an example. At the time, we bought stocks of investment firms (the likes of Janus & Invesco), but we did not buy one 5% position; we bought three totaling 5%. They were all cheap.

There’s another factor: When you manage other people’s money, you’re managing not just your emotions but theirs as well. You want your clients not to bail out at the very bottom. So you have two tiers of emotion management. That approach helped ensure our clients didn’t panic.

Why am I micro-dosing today? The political climate has changed tremendously. The last time I spoke to CFA UK was ten years ago, almost to the day—November 2015. Look at how the world has changed. This country has changed. Europe has changed. The US is becoming unrecognizable, little by little.

The political risk today—there’s much more uncertainty, many more underwater rocks that didn’t exist before. So we’ve reduced our position sizes again. Not as extremely as during the pandemic, but we have many 2–3% positions now.

Here’s one example. We own a British company, Watches of Switzerland. Half their sales come from the UK and half from the United States. One day I woke up and discovered tariffs on Switzerland had gone from 15% to 39%. Why? Trump had a conversation with the president of Switzerland. He didn’t like how she talked to him, so he raised it to 35% and added an extra 4% on top of that punishing tariff. Just like that. (After a Swiss delegation paid him a visit and gave him a golden Rolex, he took it back down to 15%.)

Those are the risks we have to live with today. This is why we’re micro-dosing—if something like this happens to one of our stocks, it does smaller damage to the portfolio.

On Living with Intention

I don’t understand the title of your talk. What does “living with intention” mean?

I just finished writing a new book. It’s not out yet, but it’s done. It’s called “What a Life!” with the subtitle “The Operating System for a Life Well-Lived.” It’s not an investment book, and there’s a whole section on intentionality.

I find—and when I say this, I’m usually speaking about myself, but it probably applies to everyone—that we often go through life physically present but mentally somewhere else.

Let me tell you a story. About ten years ago, I was in Vienna with my father. We walked through museums and then went to the opera—La Bohème. I love opera. I was in this incredible opera house, with my father, a person I love dearly, listening to one of my favorite operas in the world. And I found myself thinking about what I was going to have for breakfast tomorrow.

Think about it. I was physically there, but mentally I wasn’t. I wasn’t being present.

The punchline: My father said something that really shook me up. He said, “You always want to be somewhere else. You always want to be in the next place.”

I think we do this a lot. Intentionality is, first of all, being present where you are.

We often do things on autopilot, mindlessly, not intentionally, because we’ve done them for so long. Sometimes we act without thinking. When you’re intentional, you’re present in what you think and what you do.

On the Boiling Frog Problem

For value investors, the boiling frog problem is probably the most difficult thing we face. You do the work on a stock; you think you understand it well. Something goes a little wrong, but you think it’s fine. It goes down. More bad news. Drip, drip, drip—and before you know it, you’ve lost a lot of money. How good are you at coping with that and getting out quickly enough?

That is such a great question, and a very painful one.

It’s very difficult. Ideally, you think a company is worth X amount of dollars, you’re paying less than X, a discount. Problems happen. The value declines, the price declines. But there’s still a margin of safety… or is there?

I’ve made several adjustments over the years. First, I’m obsessed about the quality of companies we own. Let me clarify what I mean. I’m a very different investor today than I was three, five, or ten years ago. That’s a good thing—it means I’ve actually learned something.

In the past, when I talked about quality, I would mention competitive advantage, return on equity, return on capital, balance sheets. Those things are still true. But today I’m also obsessed about the people running the company.

I also make sure—especially today—to avoid any possible structural changes where technological change makes a company obsolete.

Today I spend so much more time thinking about management: how they allocate capital, how they run the business. We spend huge amounts of time talking to competitors, reading transcripts from interviews and expert networks.

Despite all this, I’ve reduced the problem but not eliminated it. It’s still going to happen. And you know what? When I realize it’s happening, I sell.

Here’s one thing I’ve found: At that point, the position starts consuming enormous mental real estate. What used to be a 3% position is now 2%, but it’s consuming 15% of my mental bandwidth.

Another adjustment: waiting for fundamental momentum. One of our largest positions is Babcock, a British company. We increased the position substantially when we understood how great the management is and when the business started to turn.

The old me would keep buying on the way down. The new me is more patient, waiting for signs the business is turning. If it’s a turnaround, I wait for evidence before making my position larger. The combination of these approaches helps—but I’m still not going to avoid all the boiling frogs.

Is Value Investing Dead?

Is value investing dead? The most successful investors I’ve talked to recently have been thematic investors. They buy defense companies, tech companies. They don’t care about P/E ratios. It’s themes, trends, momentum—not value.

That’s easy because I have an answer. Here’s the thing: It depends on how you define value investing.

If you define it as buying statistically cheap stocks—yeah, maybe that’s dead. Price-to-book doesn’t work for analyzing Microsoft or any software company. When I started investing, I thought value investing was just buying cheap stocks. That’s what you learn if you read Ben Graham’s books and get one-tenth out of them. You get the cookbook stuff but not the philosophy.

Value investing is not about buying cheap stocks. Value investing is a philosophy. In fact—and this is not me, this is Buffett saying it—the term value investing is redundant.

Let me explain. Value investing is several things. Analyzing stocks as businesses. Asking for a margin of safety—if you’re buying a dollar, you don’t want to pay $1.20, you want to pay 50 cents. Having a long-term time horizon. Knowing the market will be volatile and will have an opinion on your stock every single day, and taking advantage of that.

What I just described isn’t really “value investing.” It’s just investing.

One of our largest positions is Uber. It did not look like a value stock when we were buying it. But Uber’s earnings were growing; and if you look at earnings five years out, it looked significantly undervalued. It wasn’t statistically cheap based on near-term earnings, but it was undervalued. There’s a huge difference.

Value investing is dead if you define it as buying statistically cheap stocks—algorithms will arbitrage that away. That’s first-level thinking. What I described, value investing, is not dead, because common sense is not dead.

So we shouldn’t read Ben Graham anymore?

No, you should. But when you read Ben Graham, get the philosophy out of it. The formulas—buying things at six times earnings—that stuff is obsolete. If Ben Graham were alive and wrote a new book, he’d probably spend a lot less time on formulas and more time on the philosophy.

On Macro Themes, Geopolitics, and Noise

How should investors think about big themes—macroeconomics, geopolitics, tariffs? Is it noise, or are these important factors to consider?

First, you need a long-term time horizon. A lot of things will be noise; a lot won’t be. The key is figuring out which is which. I know that’s a vague answer, but the key, really, is separating noise from signal and making adjustments.

An example: Looking at the geopolitical situation, we made a decision years ago to position our portfolio toward European defense. These companies were very cheap, so if I was wrong, I’d still be okay. But we saw how geopolitics were changing and incorporated that into our portfolios.

Seth Klarman had a great quote I try to live by: “We invest micro but worry macro.”

That doesn’t mean I try to figure out interest rates six months from now. But I look at the US having $36 trillion in debt, running 6% budget deficits during supposed economic expansion, and think: God forbid we have a recession—we could be running 10% deficits. So when I structure the portfolio, I think the chances of inflation are much higher, and I make adjustments.

Today you need acute awareness of what’s going on around the world and in geopolitics. And you need to figure out what’s noise and what isn’t. How does one do that? I don’t have a formula. It’s judgment.

Reconciling Intentionality with Long-Term Investing

Living in the present rather than the future sounds like a Zen idea. Is this difficult for an investor, since we’re focused on long-term thinking, deferred gratification, and patience? How do you reconcile those two ideas?

I’ve never tried to reconcile the two… let me try in real time.

Actually, I’m not sure there’s a conflict. But let me think about where the issue might arise.

The issue in investing becomes important when you start taking things that aren’t axioms as axioms. Here’s an example: In 2006-2007, I remember hearing the words, “Real estate in the United States has never declined nationwide.” That became an axiom. Everyone made decisions as if it were a law of physics—but it wasn’t.

As an investor, it’s critical to see through that. Being intentional means identifying these underlying assumptions and saying, “Well, this hasn’t happened in the last 50 years, the last 100 years—but that doesn’t mean it can’t happen.”

Being intentional about this—identifying assumptions—is extremely important. The opposite of intentional is mindless. When you’re mindless, you accept things as they are without realizing you’re walking on thin ice while everyone else thinks it’s solid ground.

On Investment Labels and ESG

Has your definition of value investing changed over the last two or three decades, given changes in market dynamics and politics?

Over the last 20, 30, 40 years, this industry has been invaded by consultants. If you’re a consultant, I’m sorry—I’m going to offend you in a second.

When you’re a consultant, you deal with a lot of data. You start labeling things, putting them in quadrants, dividing and slicing. This is how you justify your existence. You go to a boardroom, make a PowerPoint presentation with slides, boxes and charts. I’m empathetic—I get it. So you end up with GARP, small cap, mid cap, all these labels.

To me, all this stuff is mindless noise. Either a company is undervalued or it’s not. Either it’s a high-quality business or it’s not.

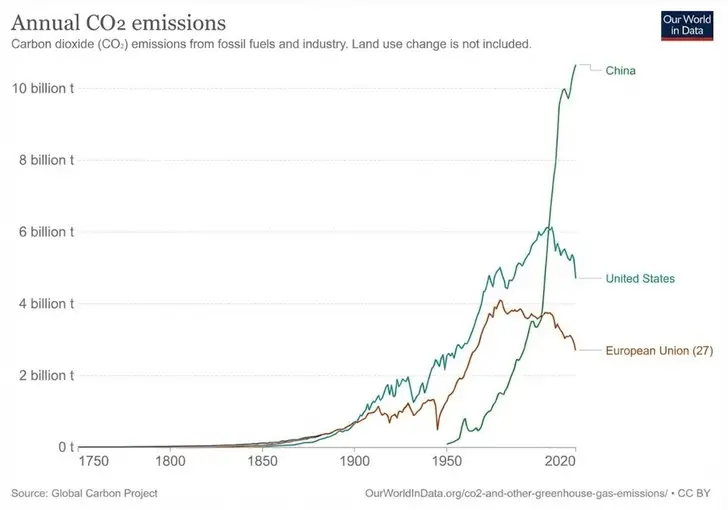

And since I’m in Europe, I’m going to upset another group: ESG. I’m sorry, but it’s nonsense, at least when it comes to investing.

I saw a chart showing CO2 emissions in Europe declining. Right next to it was China’s CO2, rising exponentially. Europe produces less CO2, but Chinese emissions have gone up enormously. The total amount of CO2 in the world hasn’t changed—actually, it went up—except now your electricity costs in the UK are four times higher and you have fewer jobs.

As an investor, I have the luxury of not voluntarily placing myself in a box, not having to worry about labels. When I was buying oil stocks and nobody wanted them because of ESG, that created an opportunity. If you owned those stocks at a mutual fund, you got fired or told not to buy them.

A lot of times, these labels create opportunities for investors. I try to take advantage of them.

The market has also become more short-term-oriented. People are less tolerant of volatility. If you have a longer time horizon and have a client base that can tolerate it, you can do better than others.

We own tobacco stocks. We own oil stocks. And whatever else isn’t ESG-friendly. My clients sleep well at night. Some of these companies have net cash balance sheets, great cash flows, and huge dividends. I just take advantage of those inefficiencies.If you are outraged about what I just said, read this.

Part 2: Artificial Intelligence, Nvidia, and the Risk of Overinvestment

On Intangibles and AI in Investing

A large portion of business value today comes from intangibles rather than hard assets. What do you think about that, and how are you navigating AI?

I’m going to answer two questions—the one you asked and the one I want to answer.

First, on AI: If you embrace it, AI can make you smarter. If you look at AI as a tool, it becomes your friend. If you outsource your thinking to AI, it can make you dumber.

Thirty years ago, I had very good handwriting. Then personal computers came, I started typing, and today I can barely write by hand. That skill atrophied.

Today I see people outsourcing writing to AI. It worries me, especially for my kids—they’re going to forget how to write. That’s a huge negative.

But AI can also be your sparring partner. You can debate a stock with ChatGPT, and that makes you smarter. It helped me edit my book—usually you send a draft to an editor and get it back two days later. Now I can have an editing process in real time. I’m still doing the writing; AI is helping me edit.

We use AI in our research process, but carefully. We don’t want AI thinking for us—we want AI helping us think.

Here’s an example: I still read or listen to conference calls. But say I’m looking at a company for the first time and want to understand what happened over the last ten years. We download transcripts of earnings calls, throw them into ChatGPT, and say, “Tell me how management’s narrative has changed over the years.” I get a page-and-a-half summary. Before, that would have taken me a week reading 500 pages. Now I have new data that wasn’t accessible before.

Another example: A company claimed their prices were much cheaper than competitors’. I asked ChatGPT to compare their prices to every competitor, and it actually went to websites, navigated menus, and selected options. Twenty minutes later, I had a table listing all the prices.

On intangibles: Yes, the economy has changed. We’re becoming more of a knowledge economy. And the scary part is the speed of change. I look at Google and have no idea what its future looks like. I have friends who are very bullish on Google—they have good reasons. Google has TPU, their own processor, much cheaper than Nvidia. They came out with Gemini, which is supposedly phenomenal.

But three years ago, nobody questioned whether Google Search would remain a monopoly. Today it has competition that wasn’t there before.

A lot of times I look at these things and don’t have an answer. I wrote an article about this: Today everyone feels they have to have an opinion on every Magnificent Seven stock. I look at them and really don’t know—and by the way, a lot of them aren’t cheap.

But here’s what’s liberating: I have a portfolio of 25, maybe 30 stocks. There are 10,000 stocks out there. I don’t have to own Magnificent Seven stocks. I just need 25, and I have 10,000 to choose from.

So I can look at a company and ask: Is AI going to change this business? Benefit it? If I have no idea, I just move on to the next stock.

Is There an AI Bubble?

Now I’ll answer the question I’ve been waiting for. I expected it five questions ago. Is there an AI bubble?

I’ve thought a lot about this. I break it into a few parts.

From a stock perspective: look at Nvidia. Its income statement looks like a software company’s—maybe 75% gross margins (for context, Microsoft’s gross margins are 69%, Salesforce’s 78%).

Another data point: Intel at its peak dominance, when it was king of the world, when every computer and server ran on its chips, had max pretax margins of 32%—and only for a few years. Nvidia’s pretax margin today is 62%.

This is because Nvidia is essentially the only company making GPUs, outside of AMD and a few from Google. So they can charge incredibly high prices.

The problem is there are startups working on competing products. And then you have Google, Meta, Tesla—all the companies paying Nvidia billions—working on their own chips.

If capitalism works, Nvidia won’t be the only GPU provider forever.

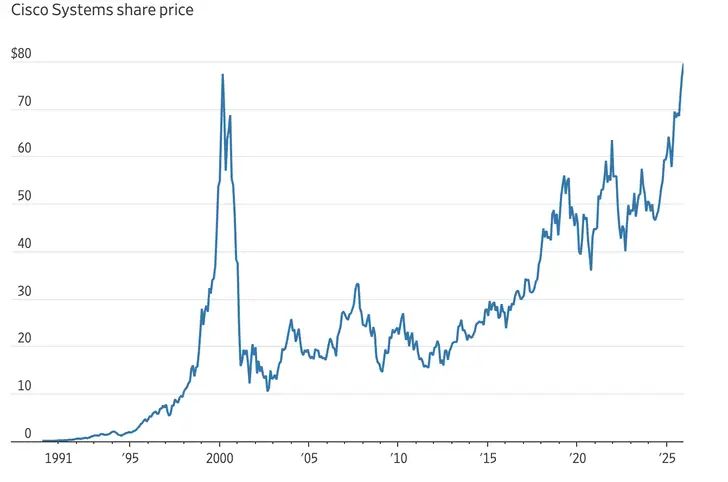

Bulls will tell you that Nvidia trades at “only” 30 times earnings.

I remember, when the telecom bubble was bursting, reading bullish articles arguing that Cisco was trading at “only” 30 times earnings. If you bought Cisco then, at “only” 30 times forward earnings—and those earnings estimates were based on pie-in-the-sky projections—it took you literally a quarter of a century, a generation, to make your money back.

Nvidia’s stock is likely going to follow a similar path.

But I don’t want to talk about earnings.

The value of any asset is the present value of future cash flows over a long period. If you buy Nvidia today, you have to be certain those cash flows are sustainable. I’d question that.

Let me tell you what’s priced into Nvidia today. I ran a discounted cash flow model: revenues doubling to $400 billion by 2027 and then growing 7% a year for 17 years, margins remaining at current levels, and cash flows discounted back at 7% a year. If you’re comfortable with these assumptions, you’ll make 7% a year—the discount rate.

But that’s actually the least interesting part. Here’s what gets interesting: Half of US economic growth over the last couple of quarters came from data centers. The rest of the economy is probably shrinking—or at best not growing. Take data centers away, and what do you have?

We probably have an overinvestment bubble. That’s where the bubble is happening.

I read today that DeepSeek, the Chinese version of ChatGPT, can generate tokens at 95% lower cost—some insane number. In my new book, I talk about the power of constraints. When you don’t have financial resources, when you don’t have Nvidia GPUs coming freely, you have to become more creative. You have to create more efficient models. That’s what DeepSeek did.

What’s happening today in AI infrastructure looks very similar to the 1998–1999 fiber optics overbuilding. Remember Global Crossing, Level 3, Qwest, JDS Uniphase, WorldCom? Those companies were at the center of fiber optics, investing insane amounts of money because people said internet demand would be huge and insatiable.

They were right—demand was huge and insatiable. But guess what? Most of those companies either went bankrupt or nearly did. Equity holders got wiped out. Bond holders lost nearly everything.

Why? When everybody invests at once, you get overcapacity. Mark Zuckerberg said it doesn’t matter if Meta overspends a hundred billion dollars—the threat of not doing it is existential. But if Google, Tesla, and Meta all do the same, and everyone does the same, you get overcapacity. Most of these investments become malinvestments.

Also, technology changes. Part of why we have so much dark fiber 25 years later is that Cisco figured out how to compress data. You need less fiber. DeepSeek-type innovations will likely make AI training more efficient, so you won’t need as much compute.

And consider this: The internet was huge, but growth went exponential in 2008 with the iPhone, putting the internet in everyone’s hands. For AI, robotics might become that moment. But my point is: The road to AI won’t be linear. It will have a lot of bumps.

But that’s not what worries me most. Here’s what worries me:

I read about Meta’s data center in Louisiana—$26 billion cost. You won’t find that $26 billion as a liability on Facebook’s balance sheet. They created a special purpose entity, put in a few billion, and it became someone else’s problem.

There’s a debate about GPU useful life—some say two years, some say three, some say six. Can we agree it’s not 24 years? Well, that data center has been financed with 24-year debt. Of that $26 billion, I promise you $20 billion or more is not concrete—it’s GPUs going to Nvidia, financed with 24-year debt. A lot of it comes from private credit.

This looks very bubbly. There’s a debt issue coming.

The pushback I get: “Usually people don’t talk about bubbles during bubbles.” That’s true. Bubbles can last much longer than you think. People like me will get sick of talking about it, and that’s when it ends in tears.

Oracle changed the AI race from being financed by cash flows to being financed by debt.

Let me walk through Oracle’s numbers. Market cap: maybe $600 billion. Free cash flows: roughly $12–15 billion. Net debt: about $80–90 billion. And they just committed to spend hundreds of billions on the OpenAI deal.

Remember: $15 billion in free cash flows. A lot of debt already. And now hundreds of billions in commitments. Larry Ellison is making an all-or-nothing bet. He’s borrowing, Meta’s borrowing, everyone’s borrowing—that’s what’s happening.

I just finished reading Andrew Ross Sorkin’s book on 1929. Highly recommend it—great insight into people. One character reminded me of someone today: William C. Durant. He started General Motors, got kicked out, co-founded Chevrolet, merged it with GM, got kicked out again. A brilliant businessman who started two auto companies.

But he speculated in 1929, got wiped out, and died destitute, managing a bowling alley in the middle of nowhere.

You look at him—brilliant, very smart—and yet he still did these dumb things and got wiped out. I keep thinking about Larry Ellison. I don’t think he’ll end up managing a bowling alley on his private island in Hawaii. But—coming back to your earlier question—you want to say, “Well, if he’s smart here, he must be smart there.” I’ve found it often doesn’t work that way.

What concerns me is that this behavior can last a long time before it ends. And I’m concerned about the financial consequences for pension funds and others doing private credit with very little thinking or underwriting. I’m also concerned about the health of the overall economy once you take away AI spending.

The Future of Asset Management

How do you see the asset management industry evolving with AI and passive investing?

Believe it or not, I think passive investing is a gift to people like us who do active management. Not in the short term, but in the long term.

The more people do passive investing, the less analysis gets done. The less analysis, the more you compete against dumb money. When I say “dumb money,” I don’t mean people who buy index funds are dumb—in fact, they were smarter than many professionals. It’s just that it’s a one-directional decision: buy everything. Very little analysis goes into valuing each stock.

Long term, I’m very optimistic because I’ll have less competition. It used to be 500 people valuing a stock; now there’ll be 20.

One thing that worries me—and I have to be honest, I contribute to this problem—is that in ten years we’re probably going to kill all the young analysts.

In the past, you’d have kids graduate from school, become young analysts. You’d ask them to read transcripts, summarize them, compare prices. Now I don’t need them—AI does the job of 20 analysts. So I’m not hiring them.

But to become an analyst, you have to go through vocational training, rise up through experience. If we’re not hiring young analysts, who comes after us? I don’t have an answer. That worries me.

But investing itself—we’re going to have to embrace AI or get run over. We have almost a full-time person now just figuring out how to bring AI into our research process. Not thinking for me—helping me think better.

Everyone who works for me, in any job, I ask to embrace AI. For however old you are, you didn’t have AI to go to before. Now when you have a question, you have a very smart assistant that can help you answer it—not thinking for you, but helping you think. You have to reprogram decades of behavior. That’s very important.

Key takeaways

- Managing other people’s life savings teaches you that real risk is permanent loss of capital, not volatility, and the first job is simply to survive and get clients to retirement.

- Micro-dosing positions is an honest response to uncertainty, a way to respect what you do not know, limit damage from surprises, and help clients stay emotionally invested.

- Over time, quality has come to mean less about ratios and more about the people running the business, because bad management quietly turns small problems into boiling frogs.

- Value investing is only dead if you define it as buying statistically cheap stocks; investing with intention is about understanding businesses, demanding a margin of safety, and thinking further ahead than the market.

- Living and investing intentionally both require presence, questioning hidden assumptions, and resisting autopilot, whether in a portfolio or in the moments that matter most in life.

")

Looking at the US economy (AI driven) and its staggering debt ceiling, which keeps growing, coupled with the AI investments, fuelled also by debt and “strategic partnerships” a.k.a money circling between a few companies, when does this debt become too much of a problem?

Very Insightful!